Monthly Returns

Pool of 3,350+Loans Originated by NBFC Backed by Accel, Ribbit, Tiger Global

Rated

Filling Fast

LoanX Moneyview Feb’26

Opportunity Overview

Benchmarking of Returns

Why Do We Like This Opportunity

Attractive Risk-Adjusted Returns

12.8 % Target IRR: Net expected returns are 120-200 basis points higher than a similar rated corporate bond

Monthly Payouts: The payout of both, interest as well as principal will be on a monthly basis

Low Average Tenure: Weighted average deal tenure\ of the underlying pool is only ~9 months

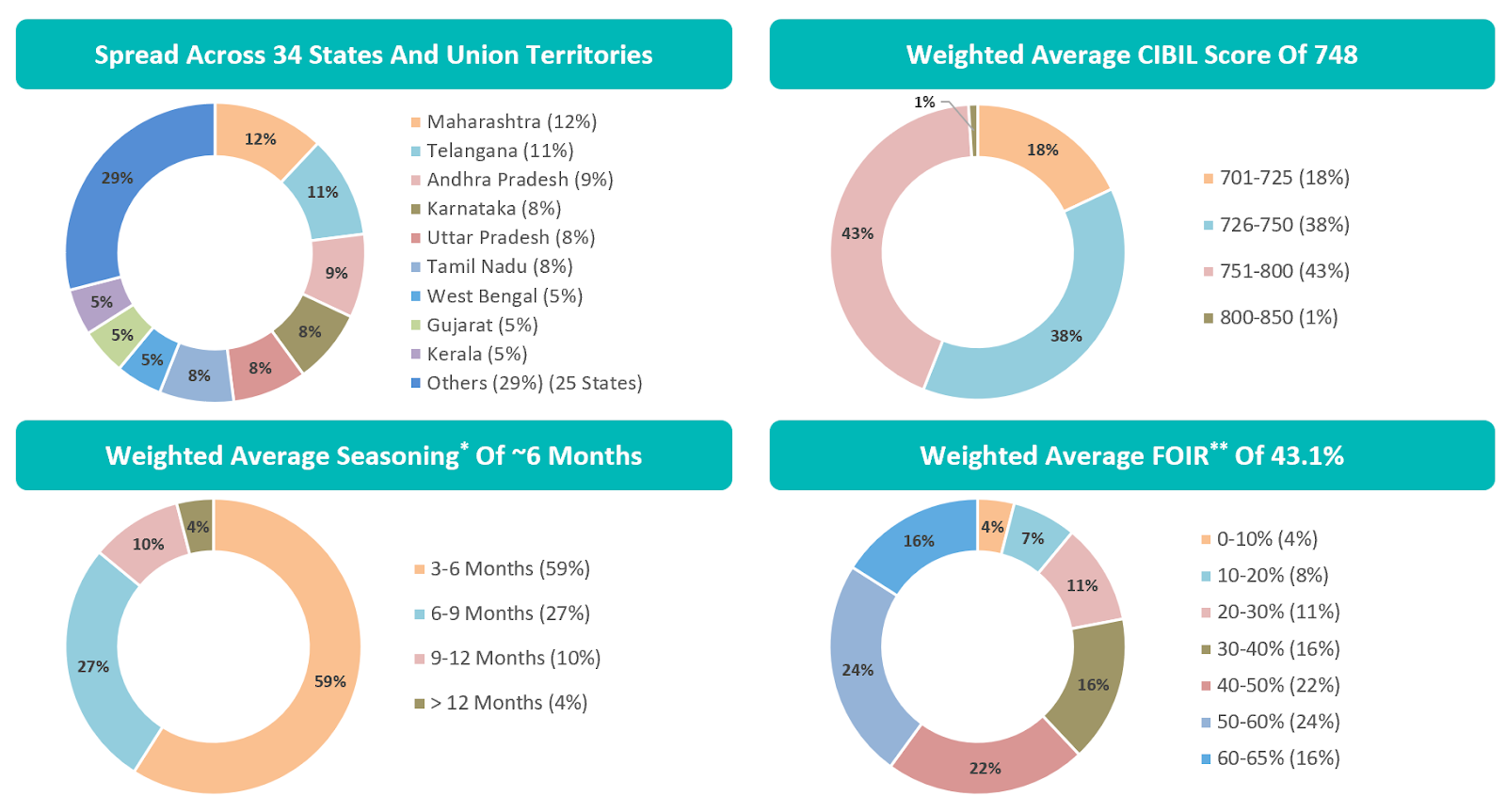

Diversified Pool With A Proven Repayment Track Record and High CIBIL Score

Diversified Pool: With 3,350+ loans in the pool, exposure per loan is INR 30 for every INR 1 Lakh of investment

Proven Repayment Track Record: The Pool has seen ~6 months of on-time repayment and no default till now

High Borrower’s CIBIL Score: Weighted average CIBIL score of the underlying borrowers is 748, with minimum CIBIL score for any borrower being 701

Low Outstanding Ticket Size: The loan pool comprises an average outstanding ticket size of INR 70,672 as of cut-off date

Robust Security Cover

Security Cover: The opportunity has a weighted average security cover of 1.38x of the investment amount

Delay/Default Coverage: Even if 60% of interest payments from the underlying loans are delayed, or if the pool defaults up to 25%, the available security cover is sufficient to protect investor’s expected IRR

Note (\): Weighted Average Deal Tenure represents average maturity of the instrument as it amortizes through its term, considering each months’ payout as weights

Details of 3,350+ Personal Loans Pooled in this Transaction

Note (\): Seasoning indicates the number of monthly installments that have already been received from the underlying loans in the pool

Note (\\): Fixed Obligations to Income Ratio (FOIR) indicates a borrower's disposable income that they can use to repay existing and new debts

Originator Overview

About Moneyview:

Moneyview is ‘BBB+’ rated by India Ratings (registered as “WhizDm Finance Private Limited”), primarily focusing on providing unsecured personal loans to salaried and self-employed individuals

Moneyview has PAN-India presence, spread across 36 states and union territories

Leadership Background:

[Puneet Agarwal, Co-Founder and CEO](https://www.linkedin.com/in/puneetagarwalindia/), is a graduate from IIT-Delhi, having an experience of over 25 years in Finance, with companies like McKinsey, Google, Capital One etc. His areas of expertise include creation and development of multiple new age financial products, fintech operations etc.

[Sanjay Aggarwal, Co-Founder and CTO](https://www.linkedin.com/in/sanjay-aggarwal-iitd/), is a graduate from IIT-Delhi, having an experience of over 25 years in the Information Technology field, with companies like Yahoo, Appian Communications etc. His areas of expertise include scaling consumer-oriented tech-based products.

[Saurav Goyal, Chief Financial Officer](https://www.linkedin.com/in/saurav-goyal-40905235/), is a Chartered Accountant with over 12 years of experience across Strategic Planning, Budgeting, Resource Mobilization, Accounting, Auditing, Investor Relations, etc. Prior to joining Moneyview, he has worked with EY and Cloudnine Hospital.

Portfolio and Financial Performance:

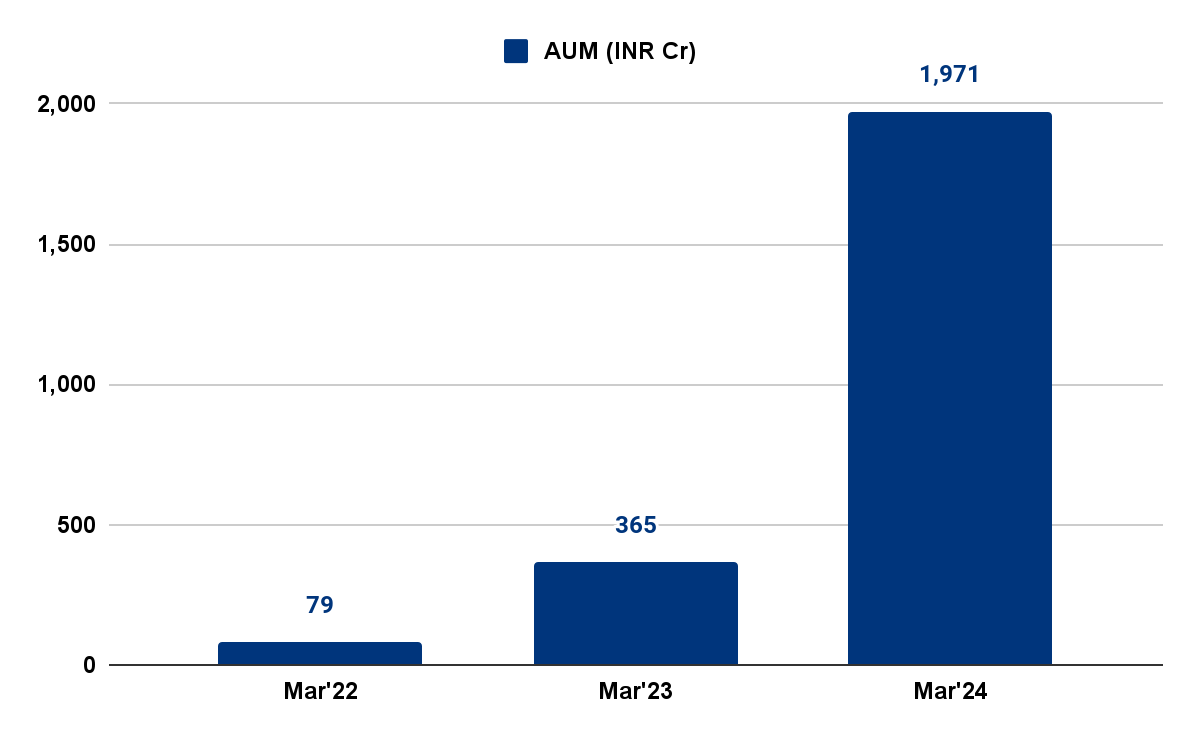

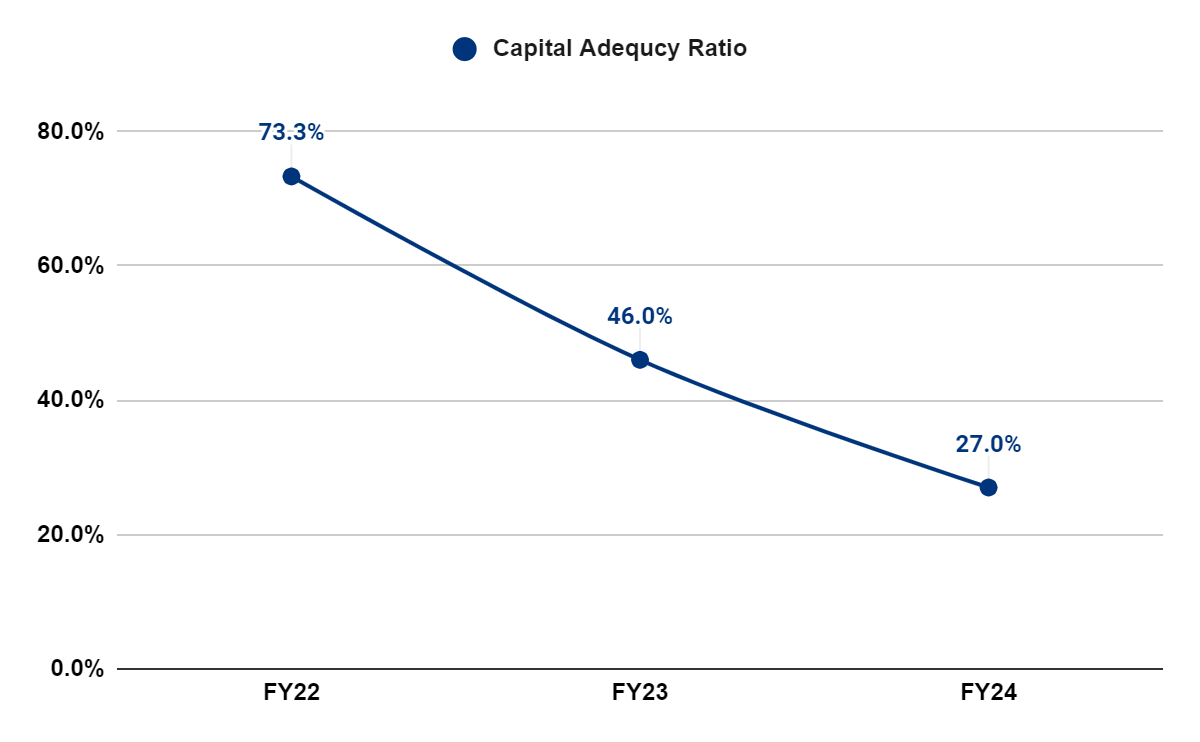

As of Mar’24, Moneyview reported an AUM of INR 1,950+ Cr

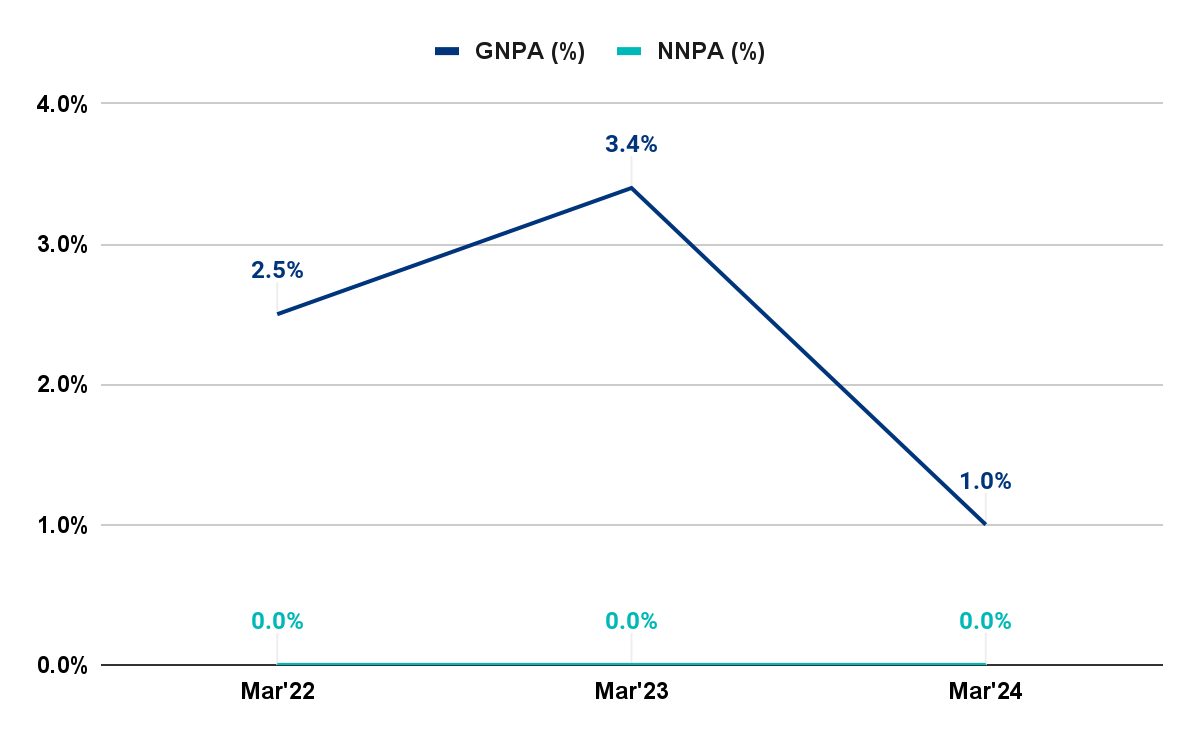

The Company reported GNPA/NNPA of 1.0%/0.0% as of Mar’24

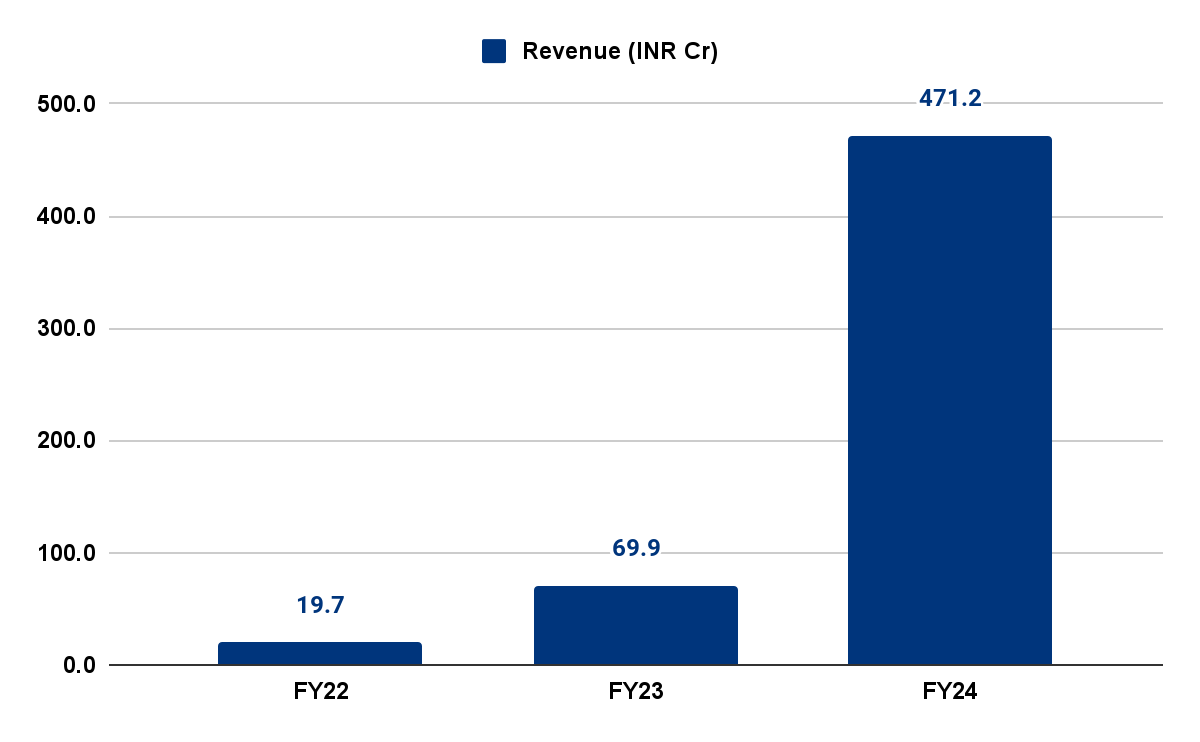

In FY24, the NBFC reported revenue of INR 471.2 Cr, with profit after tax (PAT) of INR 38.8 Cr (i.e., 8.2% of revenue)

In FY24, Moneyview reported a debt-to-equity (D/E) ratio of 2.6x, and capital adequacy ratio of 27.0% against a minimum requirement of 15% as per RBI norms

Source: Financial performance presented above are based on audited financial statements for FY22 to FY24

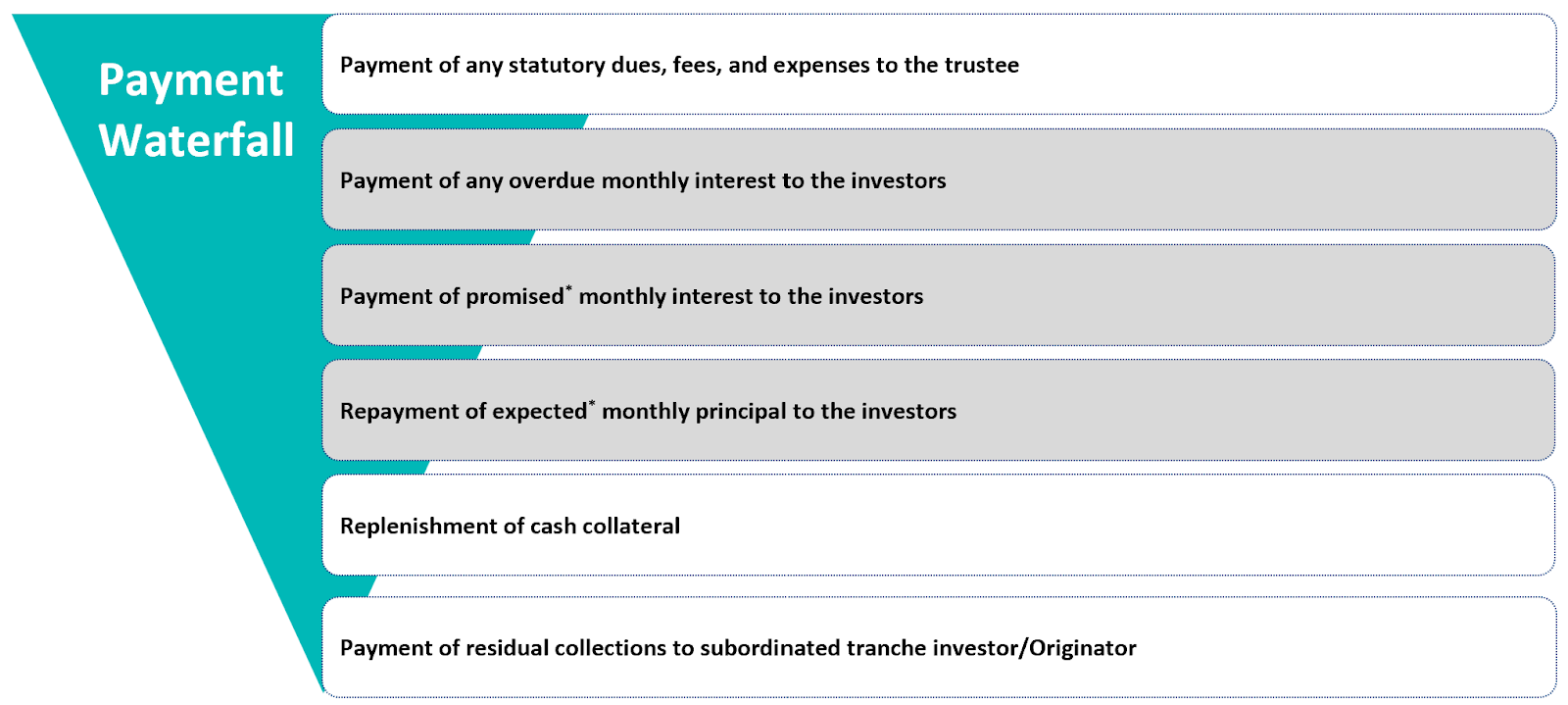

Waterfall Mechanism

Note(\): The opportunity has a timely interest and ultimate principal (TIUP) structure, wherein the interest payouts are promised, but the principal payouts are only expected. Also, if any prepayments are made by the borrowers, they will be utilized for repayment of principal to the investors.

LoanX FAQs

FAQs

What is LoanX?

LoanX is an investment opportunity structured in the form of a Securitized Debt Instrument (SDI), which is a fixed-income instrument issued in accordance with an RBI and/or SEBI framework. Grip through LoanX offers SDIs secured by a granular pool of loans such as MSME business loans, microfinance loans, joint liability group loans, loan against property (LAP), vehicle loans, etc.; these SDIs are rated by a credit rating agency. Investors/Subscribers are issued with Pass-through Certificates (PTCs) by a SEBI registered trust; which gives the rights to the investors to receive fixed monthly payouts in the form of interest and/or principal.

How is LoanX secured?

LoanX (in SDI format) is an RBI and/or SEBI complaint, and rated instrument, which is managed by an independent, SEBI-registered trustee. The returns in the LoanX originate from a granular pool of retail loans such as personal loans, MSME business loans, microfinance loans, joint liability group loans, loan against property (LAP), vehicle loans, etc. The security package of LoanX generally consists of over-collateralization, cash collateral, and excess interest spread (EIS).

Over-collateralization refers to having loans worth INR (100+x) as collateral, against an investment of INR 100. So, if in an opportunity, over-collateralization is 10%, then it has loans worth INR 110 as collateral, against INR 100 investment.

Cash collateral is in the form of an upfront fixed deposit by the originator

EIS is the difference between the interest payable by the borrowers in the pool, and the interest payable to investors

What is the tax applicable on my return?

Only the monthly interest payout is expected to be taxed at the marginal tax rate of the individual investor; no tax should be payable on the principal repayment. Appreciation (if any) of the price of the SDI, in case of sale prior to the full tenure, is expected to be considered as capital gain and taxed accordingly. Please do not consider this as tax advice. We urge you to speak with your independent tax advisor.

What is accrued interest?

Accrued interest is the amount of interest due on the SDI that has accumulated since the last time an interest payment was made. The interest has been earned by the existing holder, but because interest is only paid at set intervals the investor has not received the money yet. If the present holder sells his SDI, he should be entitled to get the interest until the date of the sale.

For example, assume you receive INR 1,000 as interest on the 30th of every month. On the 15th of the month, you decide to sell the SDI. Since you held the SDI for 15 days, an equivalent coupon amount, in this case INR 500 is earned by you but not yet received. Hence, when you sell the SDI, the INR 500 in accrued interest must be added to the sale price to fairly compensate you.

What is the difference between the clean price and dirty price of the SDI? (Purchase Price vs. Investment Amount)

The clean price is the price of an SDI not including any accrued interest. The clean price is typically calculated as the adjusted face value of the instrument closer to the nearest payout date, ceteris paribus. Dirty price is the price of an SDI that includes accrued interest between payout dates.

How is the Investment amount of a SDI calculated?

The investment amount is the sum of the face value of each SDI (“Clean Price”) and accrued interest.

Is it compulsory to do KYC for LoanX investment?

Yes, RBI has mandated KYC requirements for the purchase of the Pass-through Certificates (PTCs) to prevent money laundering activities

What level of credit evaluation and due diligence is done for LoanX transactions before bringing the opportunity on Grip’s platform?

Evaluation and filtering by the originator; the originator applies certain filtering criterias before extending a loan to any individual/group, like earnings analysis, credit bureau check, background verification, etc.

Internal evaluation by Grip, which involves; benchmarking of originator’s background and the management team with market standards; analysis of the originator's portfolio of loans to identify a pool that complies with RBI and SEBI regulations and has credit worthiness; and ensuring market standard risk-rewards are being incorporated in the transaction structure. Grip will, on a reasonable effort basis, attempt to carry out ongoing monitoring by obtaining necessary confirmations/ verifications from the originator. Typically, these pools are rated annually by credit rating agencies and downgrades in the pool quality entitle the invocation of early amortisation triggers.

External evaluation by a tier-1 credit rating agency, which involves; overall assessment of the pool of loans; evaluation of deal structure; assessing the sufficiency of credit enhancement to cover any potential shortfalls; and scenario analysis based on default rates, prepayments, etc.

Is there any recourse on the borrower for non-payment?

Originator as a lender generally builts in various kinds of recourse to respective borrowers. The recourse is legally established by suitable documents as per terms and conditions agreed with each borrower.

There is no recourse in LoanX opportunities beyond the credit enhancement available for the investors (except in opportunities wherein the underlying loans are asset/mortgage backed). Credit enhancement includes upfront cash collateral, over-collateralization, and excess interest spread (“EIS”); which will be available for investors and can be utilised in case of any shortfall in payments to investors.

What is NSE’s RFQ mechanism?

RFQ refers to the ‘Request for Quote’ platform of the stock exchange (NSE or BSE). This platform is meant for execution and settlement of transactions in debt securities (for example, corporate bonds, SDIs and other similar assets available on Grip’s platform). SEBI has mandated the use of this mechanism for carrying out transactions on online bond platforms (like Grip). Further, all transactions entered through the RFQ mechanism are also settled through BSE’s/ NSE’s clearing corporation, which is a highly secure way of transacting in Corporate Bonds and SDIs. The RFQ mechanism also provides various payment options such as UPI, Net Banking, NEFT and RTGS providing you with both convenience and payment security.

Follow this [link](https://www.gripinvest.in/faq/asset-types/loanx) for other FAQs on LoanX

Risks & Other Disclosures

Other Disclosures

All information provided in this document is based on publicly available information and disclosures made by the originator

Such investment does not guarantee that an investor will make money, avoid losing money, or indicate that the investment is risk-free.

The payment structure in this transaction is Timely Interest and Ultimate Principal (TIUP) (i.e., while the interest is promised on a monthly basis, principal is only expected)

Information provided in this document does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip is not registered with SEBI or RBI in any capacity and does not advise, encourage, or discourage its users to invest or not invest in any securities. Grip is solely an execution-only platform and does not guarantee or assure any return on investments made by investors in any opportunities sourced by Grip and accepts no liability for consequences of any actions taken based on the information provided. However, Grip's subsidiary (Grip Broking Private Limited) is a SEBI-registered Stock Broker (INZ000312836). Any investment made by an investor is solely based on his/her judgement. Investments in debt securities are subject to risks. Read all the offer related documents carefully.

Limited liquidity and price risk: There is no assurance that a deep secondary market will develop for these instruments. This could limit the ability of the investor to resell them. Even if a secondary market develops and sales were to take place, these secondary transactions may be at a discount to the initial issue price due to changes in the interest rate structure.

Limited recourse, delinquency and credit risk: The credit enhancement stipulated represents a limited loss cover to the Investors. These Series A1 PTCs represent an undivided beneficial interest in the assets and do not represent an obligation of either the Trust or the originator, or the parent of the Trust and originator. No financial recourse is available to the investors against the Trustee. Any delinquencies and credit losses may cause depletion of the amount available for the monthly expected pay- outs to the Investors. Further, although the Series A1 PTCs represent an undivided beneficial interest in the assets. The instrument carries a loss of principal risk as there are chances that an investor may not get back the money he or she has invested or may lose the value or at least a portion of the original investment made.

Prepayment risk: There could be prepayments under any of the loan agreements. The investors are subject to the risk of changes in the average tenor of the respective loans on account of prepayments.

Bankruptcy of the Originator/Servicer: If the originator becomes subject to bankruptcy proceedings and the court or tribunal in the bankruptcy proceedings concludes that the sale from the originator to the Trust was not a valid and absolute true sale, then an investor could experience losses or delays in the payments. All possible care has been taken in structuring the transaction so as to minimise the risk of recharacterisation and for the sale to the Trust to be construed as confirming to the ‘True Sale’ criteria. The legal counsel to the trust has agreed to opine that the assignment of receivables to Trust in trust for and for the benefit of the beneficiaries, as envisaged herein, would constitute an absolute and valid sale.

Co-mingling risk: The servicer will deposit all payments received from the obligor into the servicer's bank account and thereafter into the collection and pay-out account of the trust. However, as long as the originator is also the servicer, there could be a time gap between collection by the servicer in the servicer account and depositing the same into the collection and pay-out account. Further, such amounts lying in the servicer account could be construed as the servicer's assets in the event of a bankruptcy.

Receivables and borrower’s risk: The investor payouts are dependent on the timely payments of the amounts due under the loan agreements and in the event the borrower defaults to make such payments, the investor payouts may get delayed or considerably reduced or become nil. In the event of any insolvency of the borrower or on the wilful default by the borrower, the credit strength of the pool would get diluted and therefore there is a risk attached to the SDIs.

Tax risk: The investor’s pay-outs may be reduced on account of tax levies on the income distributed by the issuer to the investors, depending on the status/category of the investor, which may result in a reduction in the respective investor’s net securitisation income, if any.

For opportunities where an information memorandum/ offer document is filed with any regulatory authority, a copy of such document will be made available to you. Your attention is invited to the statement of risk factors contained under “Special Considerations and Risk Factors” (see Chapter 9 of the Information Memorandum), in addition to those listed above. Please note that the risks mentioned above are not, and are not intended to be, a complete list of all risks and considerations relevant to any products/ opportunities being made available to you, or your decision to invest in such products/ opportunities.

Other Disclosures

Issuer Name: LoanX Maple 07 2024

ISIN: INE10HV15019

Nature of Instrument: Unlisted

Seniority: Senior Tranche

Original Mode of Issue: Private Placement

Date of Issue: 29th July 2024

Rating of the Instrument: ‘A-’ by CARE, dated 26th July 2024

Face Value: INR 1,01,238 per PTC

Clean Price and Dirty Price: Based on Calculator Above

Coupon Rate: 11.90% p.a.p.m

Date of Maturity/ Tenor: 19 Feb 2026/ ~18 months

Name of Debenture Trustee: Catalyst Trusteeship Limited

Yield to Maturity: Based on Calculator Above

Offer Documents: Information Memorandum

Investment and Returns

Asset Details

This investment opportunity involves leasing out kitchen equipments, furnitures & fixtures and IT equipments to V&RO

Depreciation on the asset being leased is ~18%

Key Lease Terms

V&RO will pay a security deposit of ~13% of the asset value

Title of the assets will not be transferred to V&RO and Grip will take physical possession of these assets in case of termination of the lease

Complete compensation in case of loss of the assets will be the responsibility of V&RO. Further, they will also be responsible for all repairs (whether routine or resulting from any damage or accident and maintenance costs of the assets)

Risk Factors

All information provided in this document is based on publicly available information and disclosures made by the management of V&RO

There is no market data on the resale value of the assets being leased and in case of default by the lessee, the resale value may not be sufficient to compensate for the loss in rentals

Such investment does not guarantee that an investor will make money, avoid losing capital, or indicate that the investment is risk-free

Comparison & Returns

FAQs

FAQs

When would my returns start?

Your lease returns will start within 30 to 45 days of completion of 100% funding for an asset

In case, it takes us more than 7 days to complete 100% funding for the asset, your investment will additionally earn interest till the complete funding target is achieved. This additional interest will be paid out along with your first monthly return and be calculated at the fixed deposit rate for a 30 day FD from HDFC Bank

Is IRR different from ROI?

ROI and IRR are complementary metrics where the main difference between the two is the time value of money. ROI gives you the total return of an investment but doesn’t take into consideration the time value of money. For example, INR1,000 received today is more valuable than INR1,000 received after 3 months. IRR calculations take into consideration when the INR1,000 was received, while ROI does not.

IRR hence not only represents the amount of money earned but also how fast it was earned

What is the difference between pre-tax and post-tax returns?

For each transaction a Limited Liability Partnership, LLP is set up for the purchase and lease of the assets

Pre-tax returns are based on the lease income received by the LLP from partners. The LLP is liable to pay tax based on applicable accounting standards on this lease income. The post-tax returns are calculated after deducting such taxes as well as the management fees charged by Grip. Since there is no further tax on either the LLP or you on the distribution of these post-tax returns, these are the net returns received by you. You will have no further tax obligation or payments due to Grip from these returns.

What are the tax implications on my post-tax returns?

All payments that you receive are made post-tax and hence, there are no additional tax implications for you

Under the accounting standards applicable for LLPs, certain expenses such as depreciation reduce the effective tax rate and these benefits are already factored into your returns

How does my ITR filing process change?

As a partner to the LLP, you will need to additionally fill ITR form 3 when you submit your income tax returns

On behalf of the LLP, we will file ITR 5 and provide the same to you to make the process transparent and easy for you

Is there any repayment security and is there a contingency plan in case of non-payment by partners?

We have the ability to reclaim assets for selling or re-leasing. However, you must note that while we have these safeguards in place, it does not guarantee 100% returns in case the leasing partner defaults. In that case, Grip will take the suitable legal course

Who recovers assets in case of default?

Grip will take care of all the processes related to the reclaim of assets for selling or re-leasing

What is the process of investment?

Once the funding target is achieved, we would send you the agreement and consent letter for the LLP which would be the vehicle of investment for the deal

Parallelly, the LLP signs the agreement with the leasing partner so that the payment dates get locked

You start receiving returns within 30 days after the 100% funding is completed